Read this article in your native language (10+ supported) 👉

[Read in your language]

Is Diversification Finally Working Again?

⚠️ WARNING: Technology and investments involve risks. This is not financial advice. DYOR (Do Your Own Research).

John: 👋 Hey, Builders! Imagine you’re at a party where one guest—the U.S. stock market—has been hogging the mic for 15 years straight, belting out hits while everyone else sits awkwardly in the corner. Now, in 2025 and early 2026, the international stocks, small caps, and even emerging markets are grabbing the karaoke remote. Is diversification—that boring strategy of not betting it all on one horse—finally paying off? It matters now because after a decade-plus of U.S. dominance (up over 660% since 2009 vs. international’s 180%), recent shifts are testing if “home bias” was genius or just recency bias.[3][1]

John: Research suggests these cycles flip—every decade has winners and losers, from Japan’s 1980s boom to the U.S.’s lost 2000-2009 decade. If you’re ignoring global plays, you might miss the next windfall, as Peter Bernstein put it: diversification is an aggressive strategy because surprises come from unexpected places.[1]

Lila: Which one are you? The skeptical investor ditching international after years of underperformance? The overwhelmed DIY-er staring at too many fund options? The curious builder wondering if 2026’s early wins signal a trend? Or the time-poor pro just wanting a simple check-up?

The Problem (The “Why”)

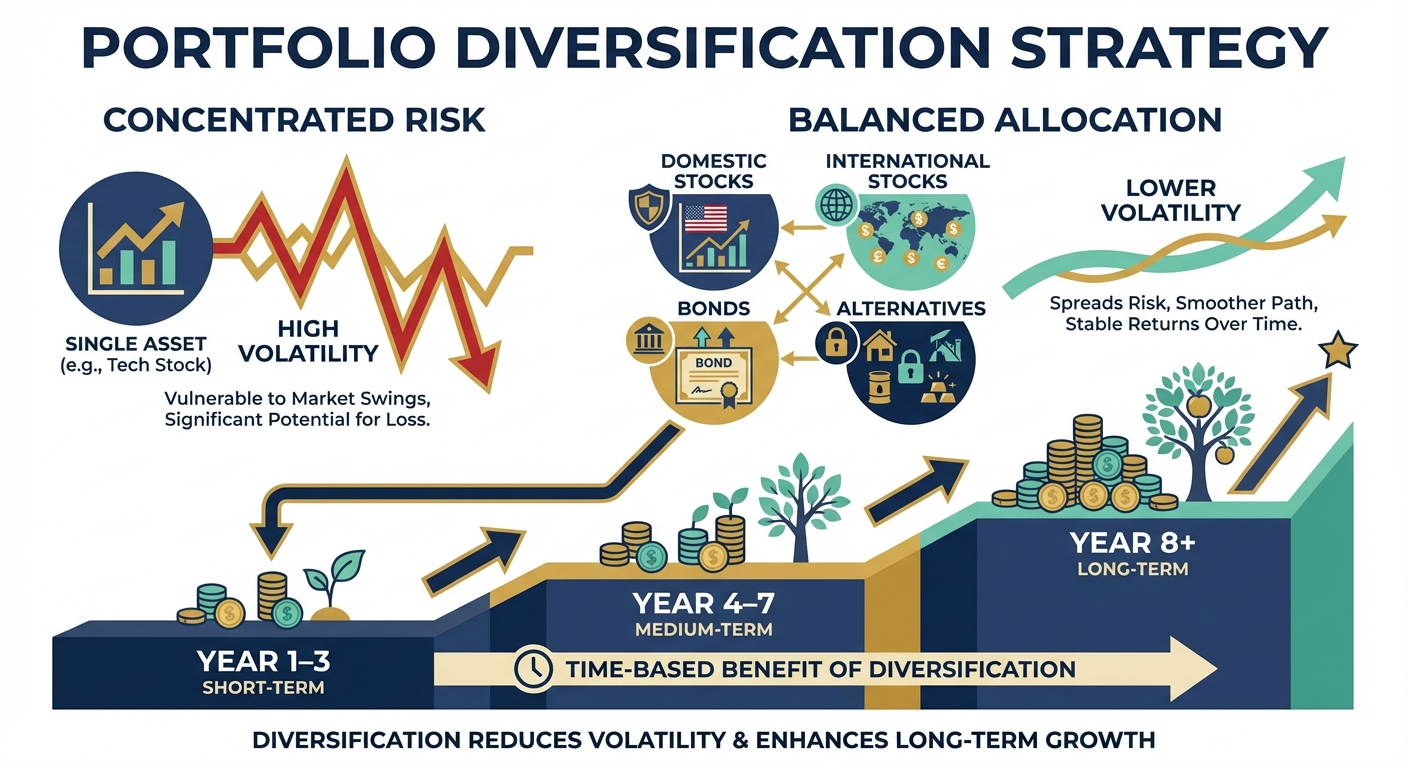

John: Picture your investment portfolio like a road trip with all your eggs in one SUV—the U.S. market. It’s been a smooth highway cruise since the Great Financial Crisis, with annual returns over 14% crushing international’s under 7%.[1] But what if that SUV hits a pothole? For years, everything outside U.S. large caps “sucked wind,” as one investor put it—international lagged, small caps struggled with debt, emerging markets boomed and busted.[3] The old way? Going all-in on U.S. giants, assuming their global sales (60% of world market cap) make diversification obsolete. Risky, because economies cycle, dollars strengthen/weaken, and no one picks the decade’s winner in advance.[1][3]

Lila: Yeah, it’s like cooking with only one spice—tasty until your taste buds go numb.

John: **Myth vs Reality:** Myth: “U.S. stocks are unbeatable forever—why bother with international?” Reality: Leadership rotates by decade; U.S. was mid-pack in the 1970s/80s and bombed 2000-2009. Practical takeaway: Diversify to dodge terrible decades, not chase home runs.[1] It’s risk management via “not knowing”—the three wisest words: I don’t know.[3]

Under the Hood: How it Works

John: Diversification spreads bets across assets that don’t all sink together—like a sports team with offense, defense, and special teams, not just star quarterbacks.[2] Core: Mix asset classes (stocks, bonds), geography (U.S., international, emerging), sectors, and low-correlation picks (e.g., gold zigs when stocks zag).[2][9] In 2025, international developed markets outpaced U.S. for the first time since 1993; 2026 YTD shows small/mid-caps and foreign leading early.[3]

Lila: Break it down in layers—I’m a visual learner.

John: **Layer 1: 10 seconds version** – Don’t bet the farm on one market; spread to smooth bumps, catch surprises.

**Layer 2: 60 seconds version** – Main chain: U.S. booms → investors pile in → overvaluation risks → dollar weakens/rates fall → international/small caps shine (as in 2025-26).[3] Low correlation assets (bonds up when stocks down) reduce volatility.[2]

**Layer 3: 3 minutes version** – Assumptions: Markets cycle (decade spreads huge).[1] Limits: Doesn’t beat top performer; adds complexity/fees if overdone (“di-worsification”).[4] Failure modes: High correlation in crashes (e.g., 2022 stocks+bonds); chase past winners and bail on losers emotionally.[3]

| Old Way (U.S.-Heavy) | New Way (Diversified) |

|---|---|

| All-in U.S. large caps: 14%+ annual since 2009, but exposed to one economy/tech bubble. | Mix U.S./intl./small/emerging/bonds: Smoother ride, caught 2025 intl. outperformance. |

| High volatility if U.S. falters (e.g., 2000s lost decade). | Low correlation reduces swings; access global growth engines. |

| Misses surprises (intl. cycles). | No home runs, but avoids strikeouts; risk-adjusted returns. |

Practical Use Cases & Application

John: Scenario 1: Retirement builder—60/40 U.S. stocks/bonds tanked together in 2022; diversified with intl./small caps weathers 2025-26 shifts better.[3] Scenario 2: Young accumulator dollar-cost averaging into emerging markets—brutal 2010-2024 (3.4% vs. S&P 13.9%), but recent rebound rewards patience.[3] Scenario 3: High-net-worth with alternatives—gold/commodities hedge dollar weakness.[6][9] Scenario 4: Career-focused pro—tilt to small caps if rates fall, aiding debt-heavy firms.[3]

Lila: But is 13 months of intl. wins a trend or trap?

John: Can’t predict—diversification shines precisely because you don’t know. It’s for decades, not days.[1]

Lila: What about fees and complexity overwhelming a beginner?

John: Start simple (total stock/bond funds); add if you understand correlations. Every holding needs a reason—expected return > inflation, low overlap.[4]

Educational Action Plan (How to Start)

John: **Level 1 (Learn):** Read classic posts on decade cycles and intl. case—track your current allocation vs. benchmarks.[1][3]

Lila: Hands-on next?

John: **Level 2 (Try Safely):** Paper-trade a diversified mix (e.g., 50% U.S., 30% intl., 10% small, 10% bonds) for 3 months; rebalance quarterly to practice discipline. Small scale only—volatility is real.

**Tiny Experiment (15 minutes today):** Goal: Spot your bias. Steps: 1) List your top 3 holdings. 2) Google “2025 asset class returns” (intl. led).[3] 3) Ask: “If this flips, am I exposed?” Observe: Emotional reaction—relief or regret? Builds awareness without risk.

Conclusion & Future Outlook

John: Tradeoffs: Diversification caps upside (no all-in on winners) for downside protection (avoids disasters); effort in monitoring vs. smoother sleep.[2][4] Uncertainty looms—U.S. AI giants could reclaim lead, or dollar drop sustains intl.[3]

**Risk Ledger:**

- What can go wrong? Correlations spike in crises; over-diversify adds fees/complexity.

- Who should be careful? Risk-averse near retirement—stick simple; speculators—size “fun money” at 5-10%.[5]

- Safest minimum: Broad stock/bond index funds, rebalance yearly.

**What to Watch Next:**

- Dollar index (DXY)—weakness boosts intl./EM.[3][6]

- Small cap vs. large cap spread amid rate cuts—debt relief or AI moat wins?

- Skill: Asset correlation tracking—free tools show if your mix zigs/zags.

Lila: Solid plan—boring but battle-tested.

John: Exactly—diversification isn’t fun, but it’s undefeated long-term.[12]

References

- Is Diversification Finally Working Again?

- Diversification is About Decades – A Wealth of Common Sense

- How to Diversify a Portfolio: A Guide to Building a Resilient Strategy

- How Much Diversification is Necessary?

- How to Diversify Against the Dollar

- A Wealth of Common Sense with Ben Carlson | White Coat Investor

▼ AI tools to streamline research and content production (free tiers may be available)

Free AI search & fact-checking

👉 Genspark

Recommended use: Quickly verify key claims and track down primary sources before publishing

Ultra-fast slides & pitch decks (free trial may be available)

👉 Gamma

Recommended use: Turn your article outline into a clean slide deck for sharing and repurposing

Auto-convert trending articles into short-form videos (free trial may be available)

👉 Revid.ai

Recommended use: Generate short-video scripts and visuals from your headline/section structure

Faceless explainer video generation (free creation may be available)

👉 Nolang

Recommended use: Create narrated explainer videos from bullet points or simple diagrams

Full task automation (start from a free plan)

👉 Make.com

Recommended use: Automate your workflow from publishing → social posting → logging → next-task creation

※Links may include affiliate tracking, and free tiers/features can change; please check each official site for the latest details.