Will Home Prices Finally Fall in 2026?

⚠️ WARNING: Investments involve high risk. This is not financial advice. DYOR (Do Your Own Research).

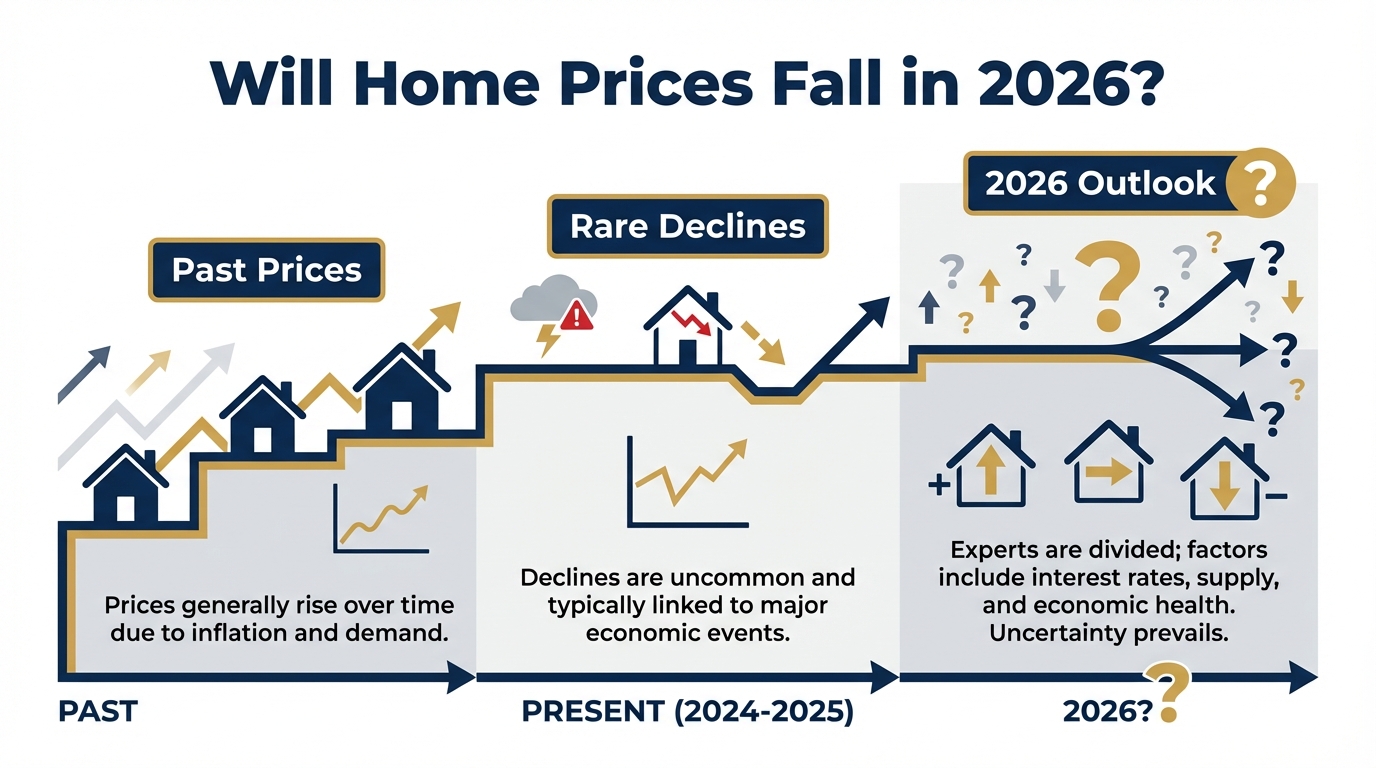

👋 Hey, Future Millionaires! If you’ve been eyeing that dream home but wincing at the price tags that seem to defy gravity, you’re not alone. The housing market has been a rollercoaster—think of it as the stock market’s more stubborn cousin, the one that refuses to crash even when everyone’s screaming “bubble!” But here’s the buzz: 2026 might just be the year things shift. Recent forecasts from experts like Redfin and Zillow suggest a potential “Great Housing Reset,” where income growth could finally outpace home prices, mortgage rates might dip, and sales could pick up. Why does this matter now? Well, with the current date hovering around late 2025, we’re on the cusp of what could be a buyer-friendly turn. After years of skyrocketing prices post-pandemic, driven by low inventory and high demand, analysts are predicting modest declines in some markets, more inventory, and affordability improvements. For instance, Redfin forecasts income growth surpassing home-price growth, potentially easing the squeeze for first-time buyers. But don’t get too excited—it’s not a guaranteed crash; think slow thaw rather than avalanche. This could reshape how we approach real estate as an asset, especially if you’re building wealth through property. Researching these trends can be a headache, sifting through endless reports and predictions. Stop endless scrolling. Ask Genspark to summarize the facts for you.

The Problem (The “Why”)

John: Alright, let’s cut through the hype. The housing market right now is like a game of musical chairs where the music stopped years ago, but everyone’s still pretending there are seats left. Prices have ballooned because of low supply—homeowners locked into ultra-low mortgage rates from the early 2020s aren’t selling, creating a bottleneck. Add in inflation, rising construction costs, and millennials finally entering the market, and you’ve got prices that feel untouchable. Lila: Totally, John. For beginners, it’s like trying to buy a ticket to a sold-out concert where scalpers have jacked up the prices. The real issue? Affordability. In many areas, home prices have outpaced wage growth by a mile, leaving young families and first-timers on the sidelines. If we don’t see some relief, it could stall economic mobility. Need to explain this concept to your team or family? Use Gamma to generate a visual presentation in seconds.

Under the Hood: How it Works

John: Let’s dive into the mechanics without the fluff. The housing market operates on supply and demand fundamentals, much like any asset class, but with unique twists like interest rates and inventory levels. Right now, we’re seeing predictions for 2026 where mortgage rates could ease to around 6.3% (per Realtor.com), potentially unlocking more buyers. Redfin calls it the “Great Housing Reset,” where income growth outpaces home-price appreciation—think 3-4% income growth vs. 2-3% price growth. This isn’t magic; it’s economics. If more homes hit the market (as “rate-locked” sellers finally move), supply increases, pressuring prices downward. Zillow predicts a modest 1.2% rise in home values, but with sales up to 4.26 million, indicating more activity. In contrast, some experts warn of declines in 22 U.S. cities, per Realtor.com, especially in overvalued spots. Lila: Breaking it down for intermediates: Factors like employment trends and inflation play in. A softening labor market could reduce demand, while lower rates make borrowing cheaper, boosting affordability. But remember, regional variations matter—Midwest markets might stay resilient due to affordability for young buyers.

| Aspect | Old Way (Pre-2026 Trends) | New Way (2026 Predictions) |

|---|---|---|

| Price Growth | Rapid increases, outpacing incomes (e.g., 5-10% annually post-pandemic) | Slowed to 1-2%, with income growth surpassing it for better affordability |

| Mortgage Rates | High (around 6.6-7%), locking out buyers | Dipping to 6.3%, encouraging more purchases |

| Inventory | Low, due to rate-locked sellers | Increasing modestly, leading to more choices and potential price dips |

| Sales Volume | Stagnant, with fewer transactions | Up slightly to 4.26 million (Zillow), signaling recovery |

| Regional Impact | Uniform pressure in hot markets | Declines in 22 cities, resilience in affordable areas like Midwest |

John: See that table? It’s not just numbers—it’s the shift from a seller’s paradise to something more balanced. But one perspective is that external shocks, like a recession, could accelerate declines, as one expert warns of a potential 50% plunge if investors pull back. Research suggests monitoring Fed policies closely.

Practical Use Cases & Application

Lila: So, how does this play out in real life? For aspiring homeowners, 2026 could mean better negotiating power—imagine snagging a house in a dipping market like those projected in overbuilt Sun Belt cities. Investors might pivot to rental properties where rent affordability improves, per Zillow. Daily life? If you’re a seller with a low-rate mortgage, consider if holding on is worth it versus cashing in before any broader dips. For portfolio builders, this reset could open doors to diversify into real estate without overpaying. John: Exactly—think of it as timing the market without gambling. One scenario: Young professionals in resilient markets like the Northeast could see stronger price holds, making it a safer buy. But consider the risks; if rates don’t fall as hoped, stagnation persists. Want to share this insight on TikTok/Shorts? Turn this article into a viral video using Revid.ai.

Educational Action Plan (How to Start)

John: Don’t just read—act. Here’s a step-by-step to navigate this.

Level 1 (Learn): Start by checking charts on platforms like TradingView or Zillow’s market reports. Read forecasts from Redfin and Realtor.com to understand local trends. Study basics like Modern Portfolio Theory to see how real estate fits into diversified assets.

Level 2 (Act): Track your local market with small habits—set alerts for price changes via apps. Test the waters with initial trials, like pre-approving a mortgage or exploring low-cost index funds tied to real estate (e.g., REITs). Remember, small, consistent steps beat big leaps. Too much text? Let Nolang explain this document to you in a video summary.

Lila: And for intermediates, dive deeper: Analyze data from sources like the Reuters poll on global trends, noting how China’s projected 3.7% decline might influence U.S. sentiment.

Conclusion & Future Outlook

John: Wrapping up, the rewards of a 2026 reset could mean improved affordability and market recovery, but risks include persistent high rates or economic downturns leading to sharper drops. Effort vs. gain? Minimal research now could yield big savings later—think sustainable wealth building over quick flips. One perspective is optimism from Redfin’s long, slow recovery view, balanced against warnings of crashes worse than 2008. Smart people automate: whether it’s health logs or price alerts, set up workflows with Make.com to save time.

👨💻 Author: SnowJon (Tech & Life Researcher)

A researcher leveraging insights from the University of Tokyo Innovation Programs to share practical wisdom on Health, Wealth, and Self-Growth. While working as a professional, he operates 8 blog media outlets & 9 YouTube channels.

His motto is to translate complex theories (whether blockchain or biology) into tools anyone can use.

*This article utilizes AI for drafting, but all verification is performed by the human author.

🛑 General Disclaimer

This article is for educational purposes only. I am not a doctor or financial advisor. Information regarding health, investments, or law should be verified with professionals. DYOR and take responsibility for your own decisions.

🛠️ Tools Mentioned:

References & Further Reading

- The ‘Great Housing Reset’ is coming: Income growth will outpace home-price growth in 2026, Redfin forecasts | Fortune

- Redfin’s 2026 Predictions: Welcome to The Great Housing Reset

- Home prices are poised to dip in 22 U.S. cities next year, a new analysis says. See where. – CBS News

- Zillow Makes 5 Predictions for the 2026 Housing Market – BAM

- Will Home Prices Finally Fall in 2026? – A Wealth of Common Sense